What's a Credit Score and How Can You Improve Yours?

A credit score is your three-digit credit history rating. Your credit score determines whether you can get approved for loans, so if you hope to mortgage a house, get a car loan, or even finance a new couch one day, you’ll want to protect and build your credit score.

But how are credit scores calculated? What’s a good credit score? How can I affect my score for the better? Below, we’ll break down these important questions.

Credit knowledge is power.

First of all, don’t kick yourself if you don’t know how all this works. A recent survey by OnePoll revealed that 71% of Americans were unaware of the ramifications of a bad credit score. But understanding what goes into it will help you build yours.

Where can I learn my personal credit score?

There are many online sources that allow you to check your own credit score using a "soft inquiry." Soft inquiries do not impact your credit score.

You can also get free scores from a number of financial institutions — including us! We offer free FICO scores to members who use our mobile app.

What’s a FICO score?

A FICO score is a specific type of credit score calculated by the Fair Issac Corporation (FICO). It’s one of a few commonly used models used by lenders. Just like your credit report may come from Equifax, Experian, or TransUnion, your credit score can be calculated in a few different ways, but the core principles are the same.

What is considered to be a good credit score?

The average credit score of a U.S. consumer is around 714. In general, credit scores tend to be lower for younger people just starting out when compared to older, more established adults. FICO’s levels of credit scoring are broken down as follows:

- Poor: 300-579

- Fair: 580-669

- Good: 670-739

- Very good: 740-799

- Exceptional: 800-850

What if my credit score isn’t so great?

If you have an imperfect past that has impacted your numbers, don’t be too hard on yourself. We’re all human, and we aren’t born with credit know-how. Damaged credit scores take effort to rebuild, but they can be improved over time.

If you haven’t used much credit, today is a good day to start. It’s a common misconception that avoiding debt will give you good credit. In reality, using credit — wisely, of course — will help you build a credit score.

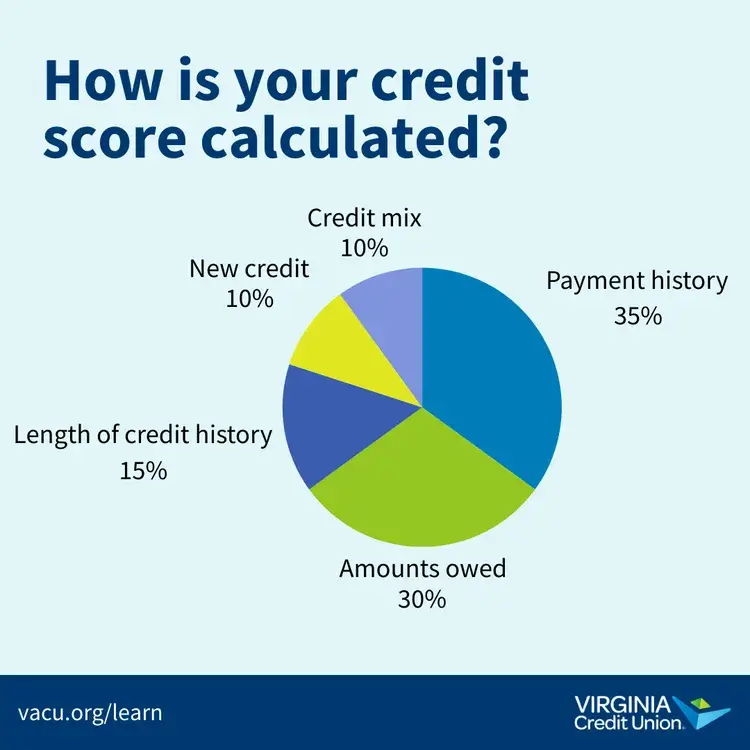

How is my credit score determined?

FICO’s calculation incorporates five major components, which are weighted as follows:

- Payment history (35%)

- Amounts owed (30%)

- Length of credit history (15%)

- New credit (10%)

- Credit mix (10%)

Let’s dive into each of these categories further and see how you can improve your score in each category.

Payment history

The largest component of your credit score is payment history, or how you are paying your creditors and how you have paid them in the past. Generally, negative information will stay on your credit report for seven years, with the exception of a Chapter 7 bankruptcy, which remains on a credit report for 10 years.

Pro tip: How can you improve and maintain your credit payment history? If you’ve missed payments, get current and stay current. The longer you pay your bills on time, the better your score.

Amounts owed

Your credit utilization ratio makes up the next largest component of your credit score. This is the total amount of credit you’re using compared to your total credit limit. For example, if you’re using $9,000 of your $10,000 credit limit, you’re using 90%. A good rule of thumb is to keep your credit utilization to 30-50% if possible.

Tips for keeping your credit utilization in line:

- Keep balances low on credit cards. Account balances should be 30% or less of your available credit.

- Pay off debt rather than moving it around.

- Pay more than the minimum required on your credit card. Large credit card balances hurt your score.

- Distribute credit card payments to keep all of your average balances low.

- Ask for credit limit increases. If you get a raise, be sure to update your creditors, as they may automatically increase your credit limit based on this new information. Incremental bumps in your credit limit can help improve your ratio, as long as you don’t use the new opportunity to rack up credit balances!

Length of credit history

The more time you’ve had credit, the better it is for your score. What does this mean? If you are just getting started, there are some ways you can start building your credit today. Consider asking to become an authorized user on a credit card account of a person with a high score. Once you open your first line of credit, have patience. Make small purchases and pay them off early or on time to start building creditworthiness. This 15% of your credit score ripens with age and will help improve your score as time goes on.

New credit

Another small but important factor in your credit score is new credit. Each time you apply for a new line of credit, whether it’s a car loan, personal loan, credit card, or other, the financer does a “hard inquiry,” and — if everything else remains the same — your score will generally drop within 30 to 60 days and rebound again. So what does this mean for you?

Apply for and open new credit accounts only as needed. And if you’re in the midst of something that depends on a good credit score — say, financing a home — don’t apply for any other credit until that transaction is complete.

Credit mix

The final component of this credit scoring model is the type of credit you have. Generally, having a variety of credit products such as mortgage loans, car loans, and other loans is preferable to having one type. Don’t worry; you don’t need one of every type. Plus, having reputable creditors such as a credit union carries weight. Learn more about our loans.

Protecting your credit

Improving or maintaining your credit score requires regular attention and patience. Be sure to deal with any collections accounts you might have, and check your credit report regularly to see if all of the information is current and correct.

Remember, in the end, you are in charge of your credit score. Understanding how it works is the first step, so give yourself a pat on the back for learning more.